For Africa to meet the intertwined challenges of demand growth and access expansion, the continent requires a massive build‑out of new generation capacity. In a new discussion paper, GET.transform and the Power Futures Lab explore the state of play, analyse where investment is (and isn’t) happening, by examining the origins of equity, debt, and EPC (engineering, procurement, and construction) investment in renewables IPP (Independent Power Producer) projects.

At the current pace, Africa is expanding power capacity at only a fraction of what is required. Under a least‑cost expansion pathway aligned with SDG7, the continent would need to add on the order of 182 GW of new generation capacity between 2023 and 2030 – roughly 26 GW every year – with about 88% of that coming from solar and wind (AfDB, 2024). By contrast, historical additions have averaged only about 7-8 GW per year across Africa, and just 2–3 GW per year in Sub‑Saharan Africa (SSA) when South Africa is excluded (EIA, 2024; BloombergNEF, 2024).

The investment gap that follows from this mismatch is substantial. The African Development Bank (AfDB) estimates that meeting generation needs and minimal associated transmission and distribution (T&D) expansion to 2030 will require average investments of around USD 64 billion per year (AfDB, 2024). Actual commitments into African power systems between 2014 and 2020 averaged about USD 35 billion annually, implying a funding gap of roughly USD 25–30 billion per year even before accounting for full grid reinforcement and last‑mile access costs.

Backed by Power Futures Lab data, the paper demonstrates that renewable IPPs offer the most practical pathway to rapidly scale investment across the continent. Investment trends show that renewable IPPs, especially in solar and wind, are driving the expansion of new generation capacity, particularly when governments and utilities face severe financial constraints.

Competitive procurement and auction mechanisms have proven effective in attracting investment and creating the enabling environment needed to unlock renewable IPP markets.

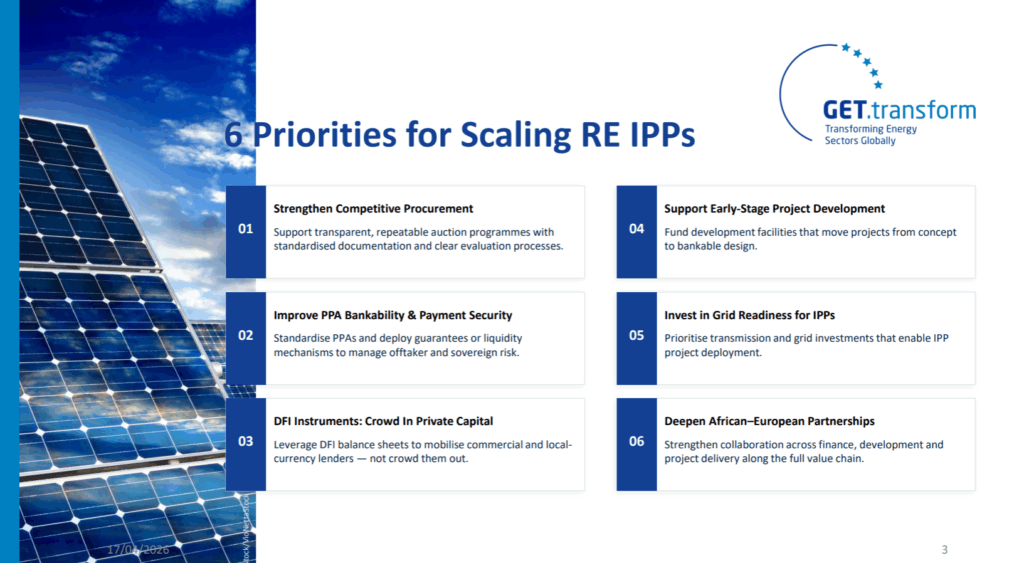

The paper highlights priorities to scale renewable IPPs. Focus should be given to strengthening the full project cycle, from enabling frameworks to delivery, establishing transparent and competitive procurement processes, improving PPA bankability and payment security. Meanwhile, DFI instruments should mobilise (rather than crowd out) private capital. There is a strong need to support early-stage project development and invest in grid readiness to ensure projects can be effectively deployed. Finally, the paper points to the importance of deepening African – European partnerships across the value chain to enhance collaboration, financing, and project delivery.

GET.transform has played an active role in bridging the gap between policy design and implementation, supporting countries in developing competitive procurement frameworks and auction mechanisms that enable renewable IPPs. Through its Policy Catalyst Effective RE Tendering Window, GET.transform provides capacity building and targeted technical assistance to strengthen IPP procurement and unlock private investment.

In addition to the current discussion paper, delve into an earlier analysis of RE auctions in Africa.